closed end credit disclosures

102621 Treatment of credit balances. Excluding chattel-dwelling-secured loans from the integrated disclosure requirements means they would not be subjected by this rulemaking to certain new disclosure requirements added to TILA section 128a by the Dodd-Frank Act.

2

See the commentary to 10265 regarding conversion of closed-end to open-end credit 3.

. 102618 Content of disclosures. 102660 Credit and charge card applications and. Sub-sections a and b cover all types of closed end transactions and then the various following subsections have specific requirements for credit sales for consumer loans for mail or telephone transactions etc.

102617 General disclosure requirements. We have a personal closed-end line of credit with a term of nine months. If any triggering term is used in a closed-end credit advertisement then the following three disclosures must also be included in that advertisement.

102619 Certain mortgage and variable-rate transactions. 102658 Internet posting of credit card agreements. Creditors may make several types of changes to closed-end model forms H-1 credit sale and H-2 loan and still be deemed to be in compliance with the regulation provided that the required disclosures are made clearly and conspicuously.

If the annual. 102657 Reporting and marketing rules for college student open-end credit. 2 The number of payments or period of repayment.

22620 Subsequent disclosure requirements. For closed end dwelling-secured loans subject to. Closed-end credit is a loan or type of credit where the funds are dispersed in full when the loan closes and must be paid back including interest and finance charges by a specific date.

22617 General disclosure requirements. Regulation Z is structured accordingly. The annual percentage rateusing that term spelled out in full.

In a closed-end consumer credit transaction secured by real property or a cooperative unit other than a reverse mortgage subject to 102633 the creditor shall provide the consumer with good faith estimates of the disclosures in 102637. 3 The amount of any payment. See the commentary to 102617 on converting open-end.

The terms of repayment. The amount or percentage of the down payment. 102659 Reevaluation of rate increases.

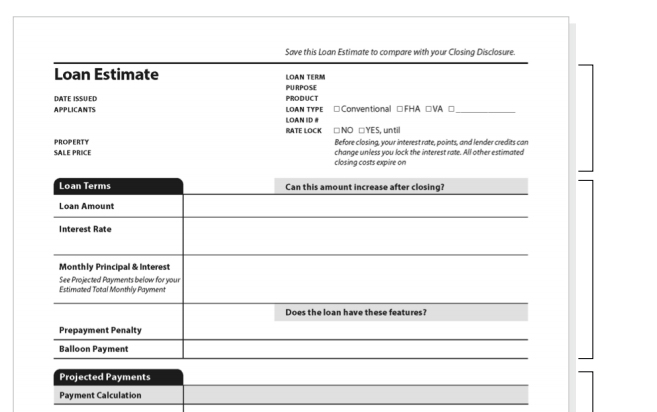

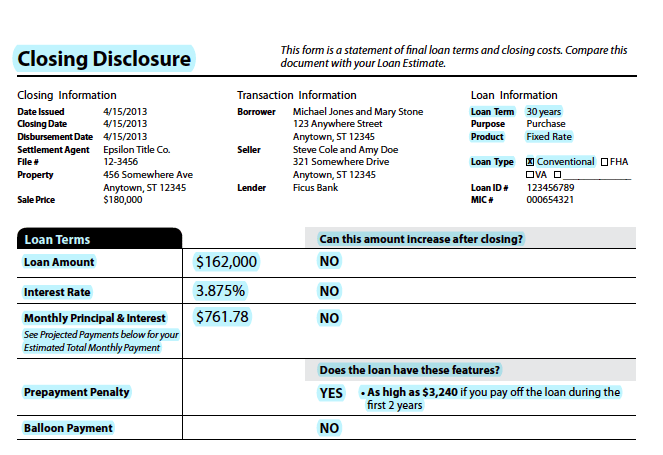

Disclosures provided on credit contracts. 2268 is the principal section for closed end credit disclosures. Closed-End Credit Disclosure Forms Transactions under 102619e f For a closed-end credit transaction subject to 102619e and f opens new window determine whether the credit union provides disclosures required under 102637 opens new window Loan Estimate and 102638 opens new window Closing Disclosure.

Accordingly the disclosures required by 102618 apply only to closed-end consumer credit transactions that are. For closed end dwelling-secured loans subject to RESPA does it appear early disclosures are delivered or mailed within three 3 business days after receiving the consumers written application and at least seven 7 business days before consummation. The disclosure rules of Regulation Z differ depend ing on whether the credit is open-end credit cards and home equity lines for example or closed-end such as car loans and mortgages.

22619 Certain mortgage and variable-rate transactions. 22621 Treatment of credit balances. If a closed-end credit transaction is converted to an open-end credit account under a written agreement with the consumer account-opening disclosures under 10266 must be given before the consumer becomes obligated on the open-end credit plan.

22619a1 and 22619a2 10. Stating No downpayment does not trigger additional disclosures. Institutions may provide disclosures required by 102624 opens new window to the consumer in electronic form without regard to consumer consent or other provisions of the E-Sign Act in.

Item Description Yes No NA. 102624b opens new windowNote. 102620 Disclosure requirements regarding post-consummation events.

102660 Credit and charge card applications and solicitations. 12 CFR Subpart C - Closed-End Credit. 102619 Certain mortgage and variable-rate transactions.

102622 Determination of annual percentage rate. 102618 Content of disclosures. We are anticipating multiple advances during the term of the credit up to the maximum amount.

The Credit Union will comply with the Truth-in-Lending Act and its implementing regulation Regulation Z by providing consumer borrowers with proper Truth-in-Lending disclosures for closed-end credit in a timely manner. Subpart AProvides general information that applies to both open-end and closed-end credit. 102661 Hybrid prepaid-credit cards.

Converting closed-end to open-end credit. The disclosures required under subsection a with respect to any open end consumer credit plan which provides for any extension of credit which is secured by the consumers principal dwelling and the pamphlet required under subsection e shall be provided to any consumer at the time the creditor distributes an application to establish an. 22618 Content of disclosures.

Does the institution make all required disclosures clearly and conspicuously. Section 102619e and f applies to closed-end consumer credit transactions that are secured by real property or a cooperative unit other than reverse mortgages subject to 102633. 1 The amount or percentage of any downpayment.

Rather they would remain subject to the existing closed-end TILA disclosure requirements under 102618. Permissible changes include the addition of the information permitted by 102617a1 and directly. Closed-End Credit Disclosure Forms Transactions under 102619e f For a closed-end credit transaction subject to 102619e and f opens new window determine whether the credit union provides disclosures required under 102637 opens new window Loan Estimate and 102638 opens new window Closing Disclosure.

Trigger terms when advertising a closed-end loan include. According to 22617 c 6 i a series of advances under an agreement to extend credit up to a certain amount may be considered as one transaction. 12 CFR Subpart C - Closed-End Credit.

Subpart C - Closed-End Credit 102617 102624 Show Hide 102617 General disclosure requirements. Or 4 The amount of any finance charge. The Credit Union will provide the proper closed-end disclosures in the following manner.

If disclosures are delayed until conversion and the closed-end transaction has a variable-rate feature disclosures should be based on the rate in effect at the time of conversion. Using a vertical rather than a horizontal.

Appendix H To Part 1026 Closed End Model Forms And Clauses Consumer Financial Protection Bureau

Mandatory Disclosures To Consumer

Fdic Law Regulations Related Acts Consumer Financial Protection Bureau

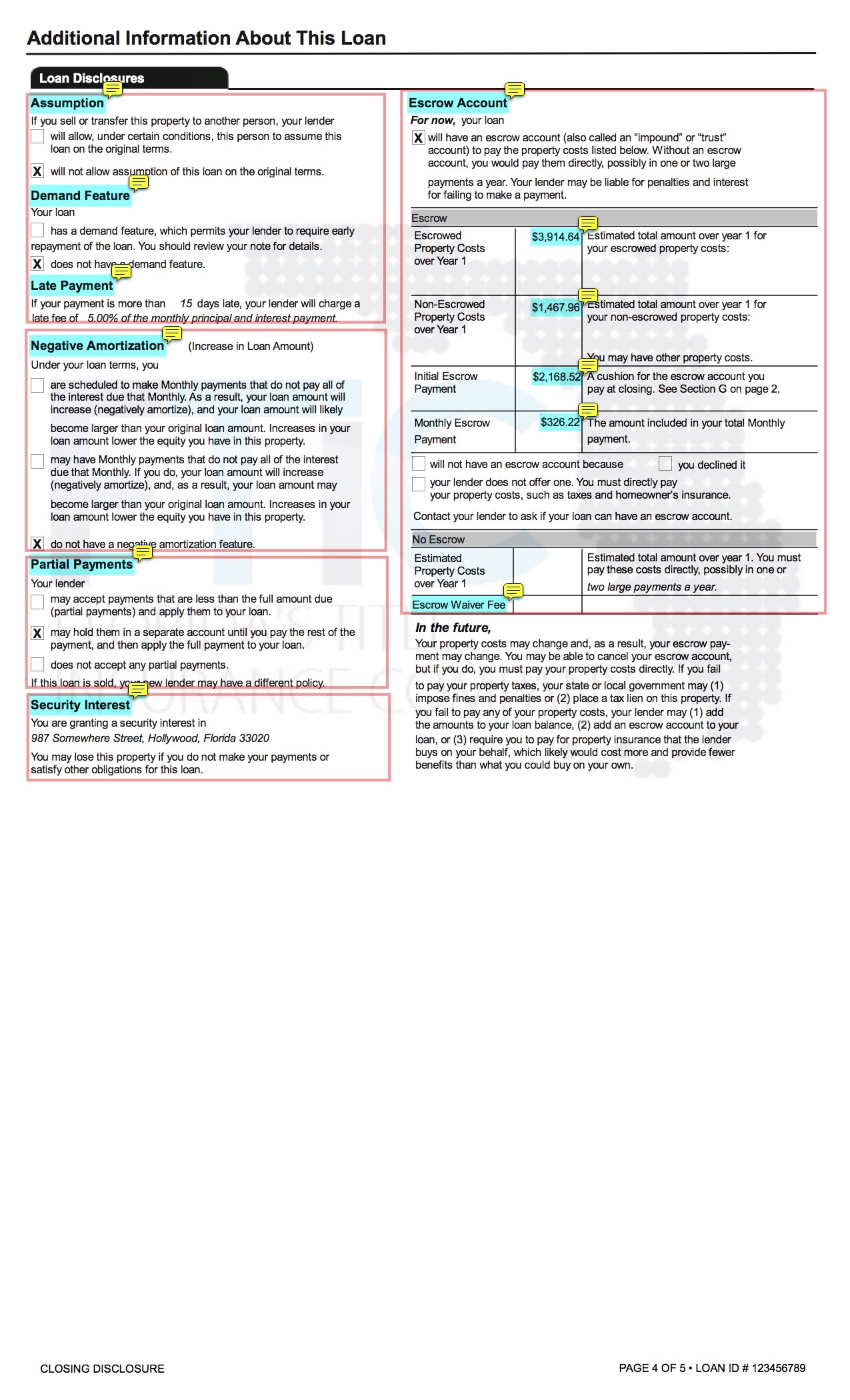

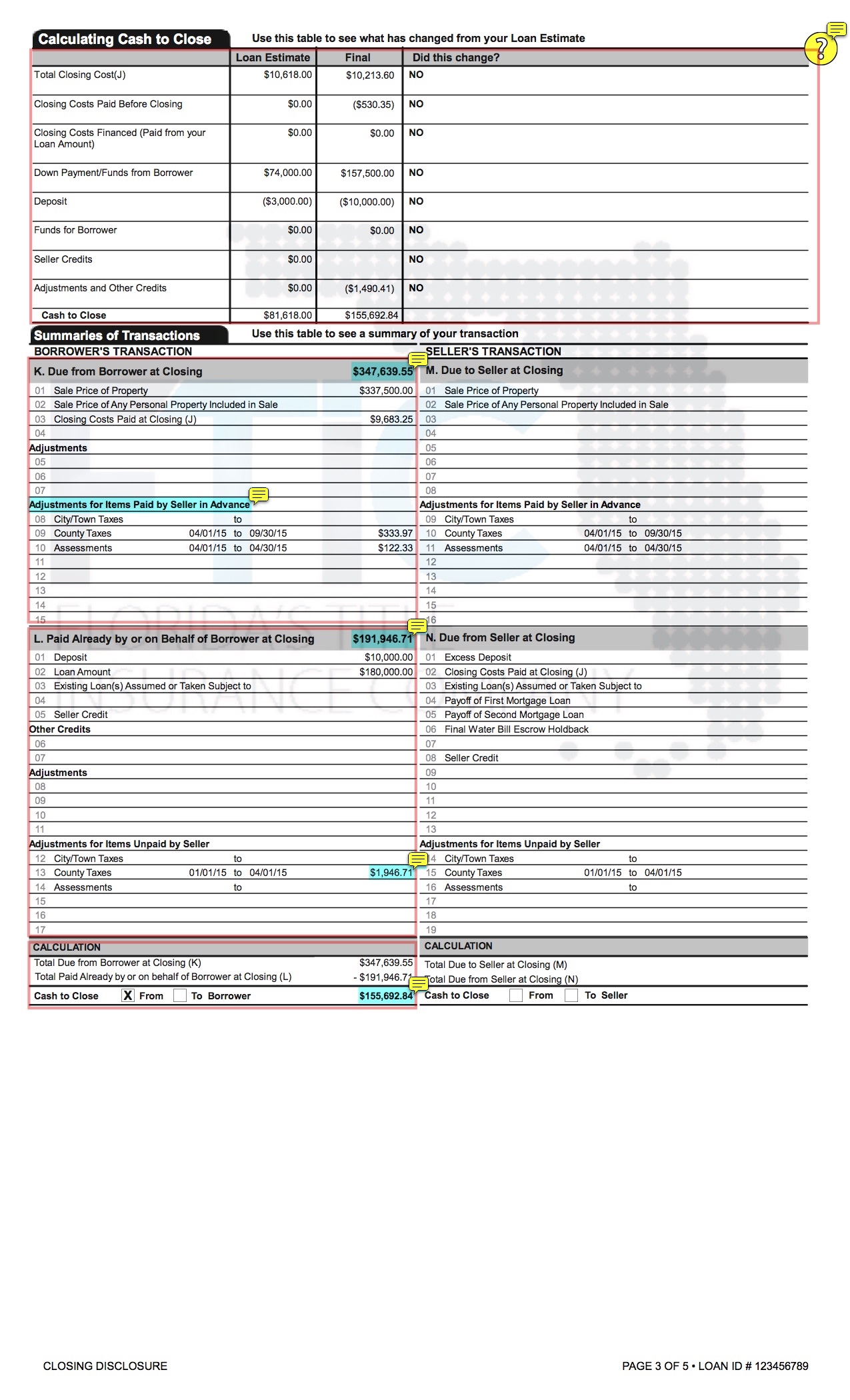

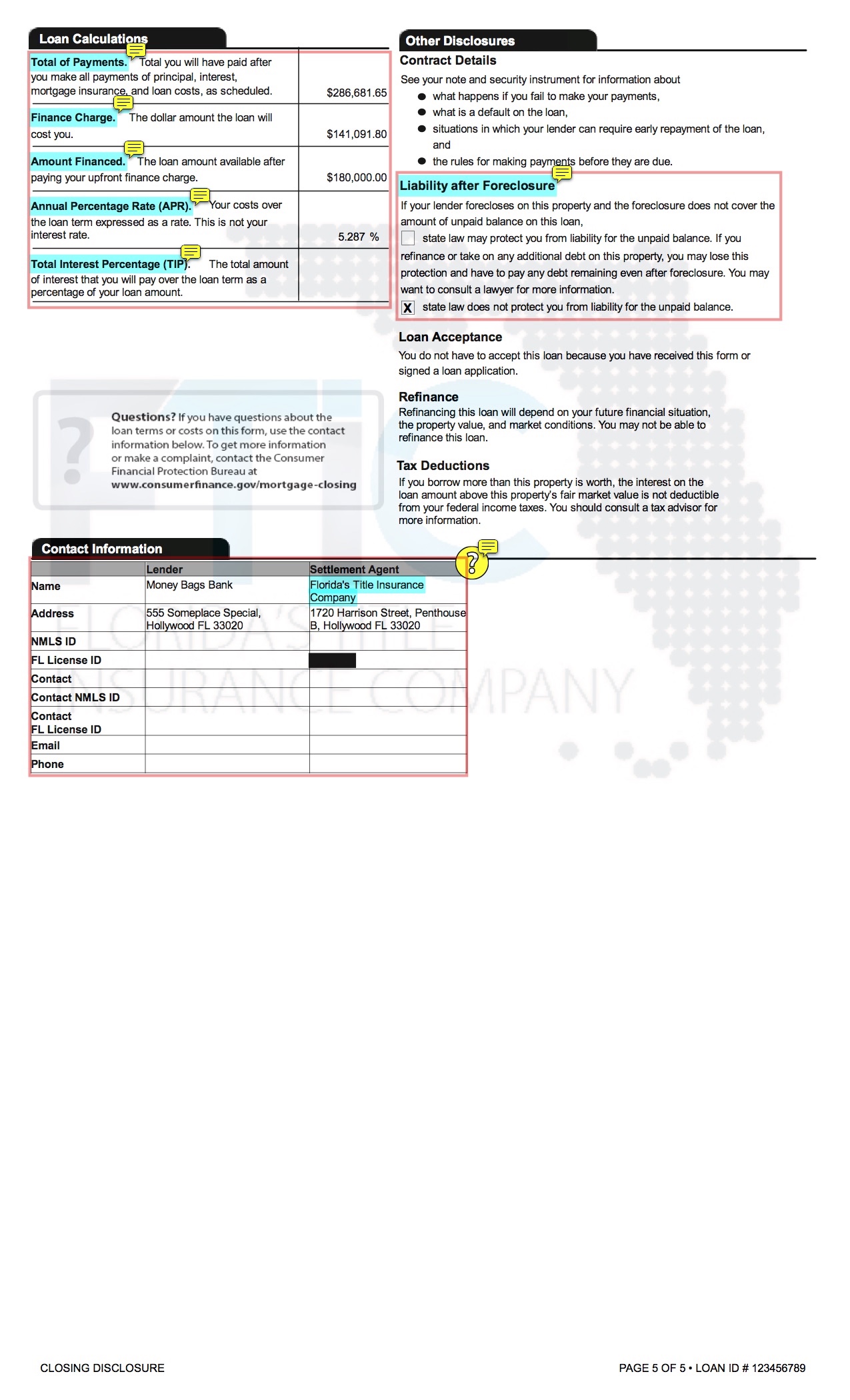

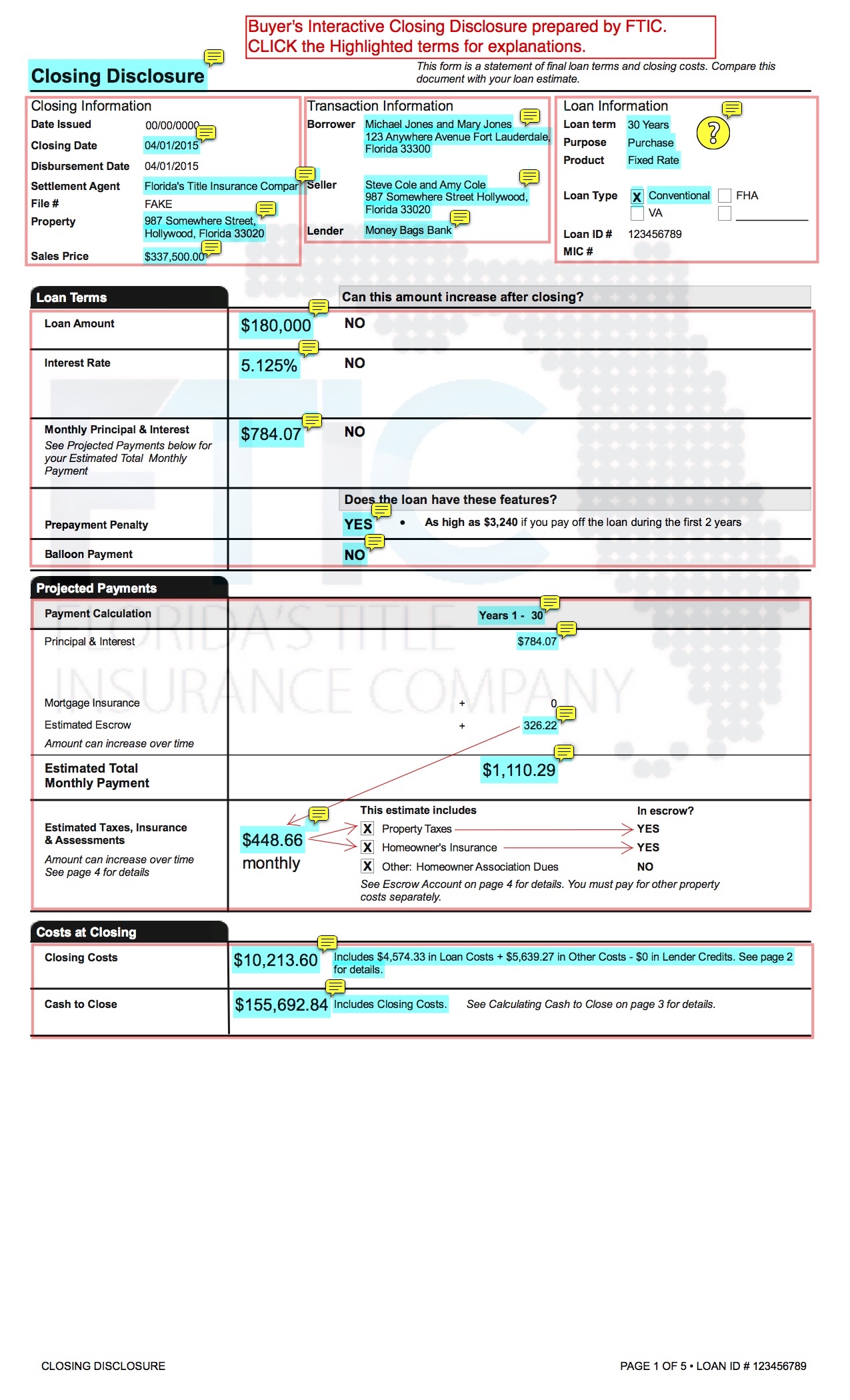

How To Read A Buyer S Closing Disclosure Florida S Title Insurance Company

Fdic Law Regulations Related Acts Consumer Financial Protection Bureau

Definition Closed End Credit Is Defined As Credit That Must Be Repaid In Advisoryhq

Appendix H To Part 1026 Closed End Model Forms And Clauses Consumer Financial Protection Bureau

How To Comply With The Closing Disclosure S Three Day Rule Alta Blog

Appendix H To Part 1026 Closed End Model Forms And Clauses Consumer Financial Protection Bureau

How To Read A Buyer S Closing Disclosure Florida S Title Insurance Company

How To Read A Buyer S Closing Disclosure Florida S Title Insurance Company

Fdic Law Regulations Related Acts Consumer Financial Protection Bureau

2

Federal Register Truth In Lending Regulation Z

How To Read A Buyer S Closing Disclosure Florida S Title Insurance Company

Understanding Finance Charges For Closed End Credit

New Mortgage Documents What Are They

Appendix H To Part 1026 Closed End Model Forms And Clauses Consumer Financial Protection Bureau

What To Know About The Loan Estimate Closing Disclosure Cd